The history of investment is fascinating - like watching a pendulum oscillate between diversification and concentration. When we look at the stock markets over the last hundred years, one thing is clear: a few companies have always dominated. But what does this actually mean for us as investors? How do we deal with this concentration?

Looking at the 1930s, we see the beginning of one of the most powerful eras of concentration. The largest stocks had market capitalizations that were seven times larger than stocks in the 75th percentile. It was a period when surviving in the markets meant relying on a handful of giant companies. While such dominance brought profits to those who bet on the right companies, it also created incredible risk.

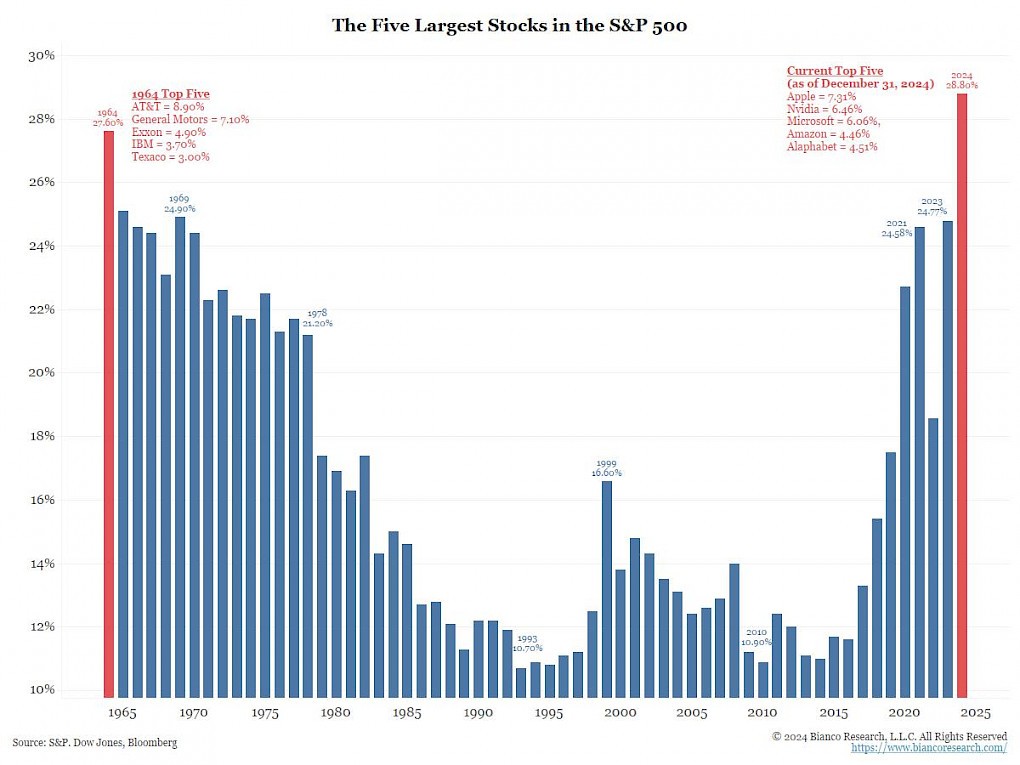

After World War II, diversification occurred. Companies like AT&T, General Motors and IBM played a key role, but markets began to include more players. The era of the "Nifty Fifty" - the 50 most important stocks - brought a kind of ideal of risk spreading. However, even then, concentration was evident. The largest companies held an important share, showing that even in more diversified periods the big players are not easily replaceable.

As we move to the turn of the millennium, we enter the world of technology. The dot-com bubble reminded us what it is like when one sector takes control. The dominance of technology companies inflated the market, only to bring about its dramatic collapse. Investors realised then that concentration in one sector could be extremely dangerous.

And today? The year 2024 shows the return of concentration on an unprecedented scale. The five largest stocks - Apple, Nvidia, Microsoft, Amazon and Alphabet - account for 28.8% of the S&P 500. That's more than in 1964. Today, it's not just about hardware or software. These companies dominate the cloud, artificial intelligence and entire ecosystems. Moreover, in the wake of the covid-19 pandemic, we are witnessing a further strengthening of their influence.

Market concentration acts as a double-edged weapon. On the one hand, it offers the possibility of making profits with relatively little effort, which can be achieved, for example, by investing in the largest companies or through the S&P 500 index. On the other hand, however, concentration increases risk because the market becomes dependent on a few players. If any of these companies encounter problems such as regulation, technological challenges or a drop in demand, the whole market will feel the impact. So instead of asking 'if', we need to ask 'when' this will happen.

It is important to remember that the window for such events is often longer than expected. Therefore, avoiding large companies may not be an ideal strategy; an investor who watches both increasing concentration and positive market developments may end up with no profit. Timing the market one hundred percent is unrealistic, and if you want to profit in this environment, you have to look for avenues that may be uncomfortable. Uncomfortable is meant in a situation where the investor is afraid to buy at the highs with such a high concentration. We often see clients like this and there is no denying that they are right. However, for someone else this strategy, as mentioned, may be the easiest and at the same time very effective way, as confirmed by the performance in recent years on the MAG 7 or the S&P 500 index.

It is likely that over the next ten years the S&P 500 may lose focus and therefore performance, which has happened with regularity in history. Historical data shows that periods of high market concentration have often been preceded by subsequent periods of declining concentration, which can result in a reduction in the overall return of the index. Yet in recent years, more than 90% of the S&P 500's return has come from the ten largest companies, suggesting that the market has become highly dependent on the performance of these firms.

If we look at historical trends, we can see that the S&P 500 index has gone through periods of stagnation and decline in the past, for example between 1969 and 1981 or during the financial crisis in 2008. These cycles show that investors should be cautious and take into account the risks associated with high concentration and potential market corrections.

For example, in our Balance product, we try to avoid excessive concentration, but not to ignore it completely. We diversify the portfolio based on current market events and look not only at the biggest players, but also at sectors and regions that may offer growth potential without undue risk. We believe that a balanced approach and thorough analysis are the keys to long-term success. We know that there is always an opportunity in the market and there is always a way to monetize any developments that arise. This is what we strive for at Balance.